Cash Receipt Journal Definition, Explanation, Format, and More

Keep in mind that your entries will vary if you offer store credit or if customers use a combination of payment methods (e.g., part cash and credit). And, enter the cash transaction in your sales journal or accounts receivable ledger. The credit sales which the busy ones make are not recorded in the cash journal as no cash is received while these sales transactions occur. Cash sales, on the other hand on a cash basis of accounting and therefore are recorded in the cash journal.

Time Value of Money

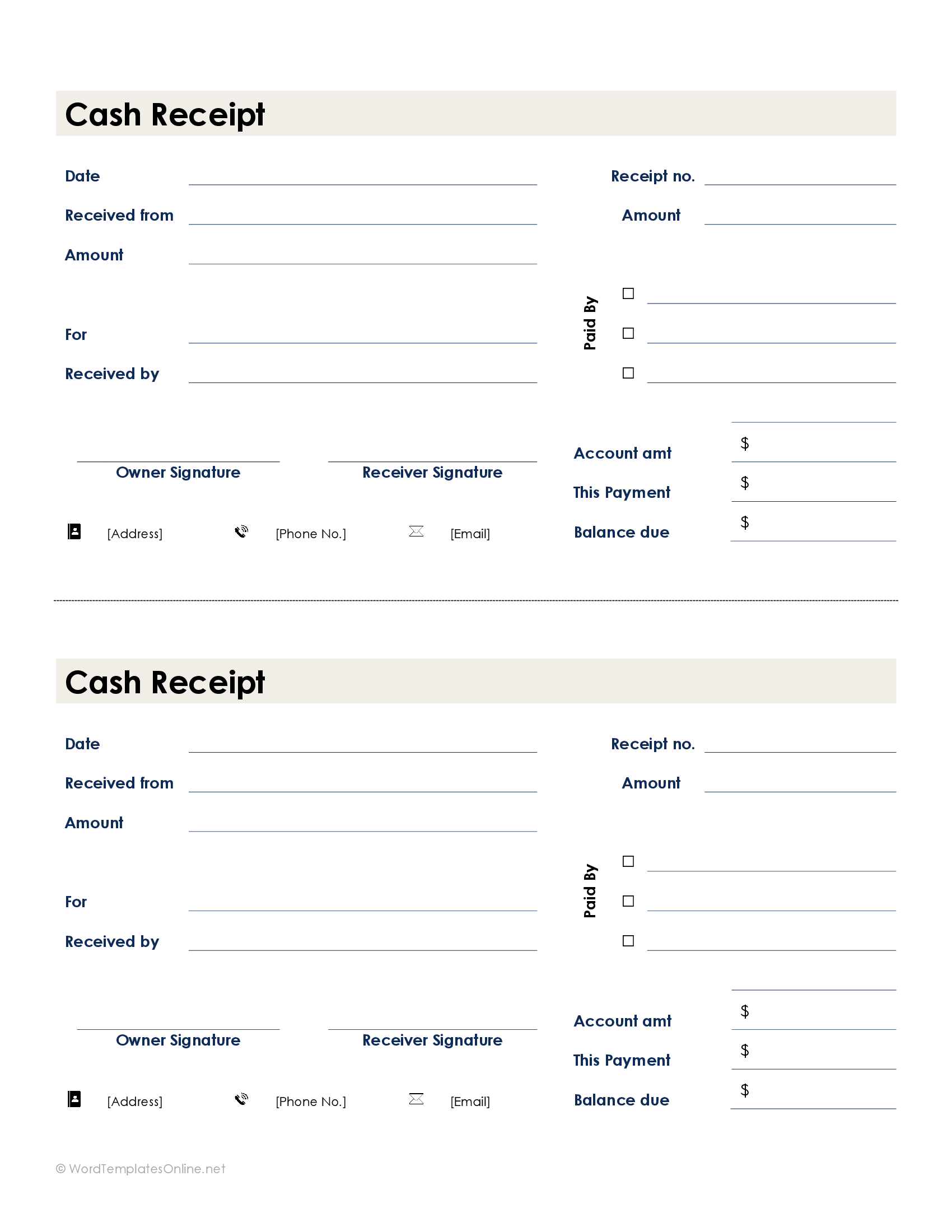

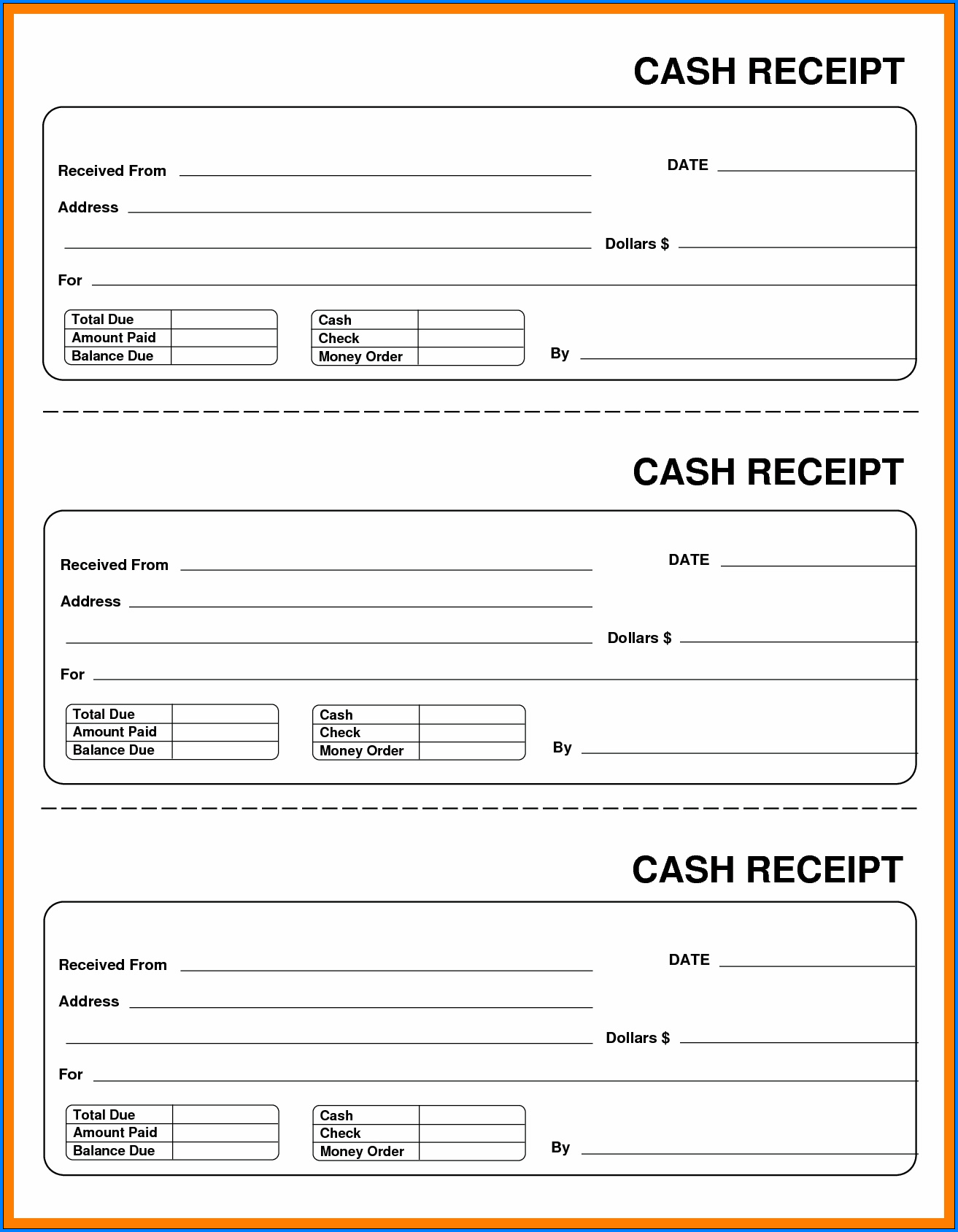

The debit columns in a do i need to file a tax return for an llc with no activity will always include a cash column and, most likely, a sales discount column. Other debit columns may be used if the firm routinely engages in a particular transaction. This format in effect combines both two column formats discussed above in that it uses the additional columns to record both discounts and bank account transactions. The first three columns in the diagram are the date, transaction description (Desc.), and ledger folio reference (LF). The single column referred to in the name of this cash ledger book is the monetary amount of the cash receipt (Cash) highlighted in gray. The cash receipts journal is that type of accounting journal that is only used to record all cash receipts during an accounting period and works on the golden rule of accounting – debit what comes in and credits what goes out.

Posting Cash Receipts Journal to Ledger Accounts

The following example illustrates how a cash receipts journal is written and how entries from there are posted to relevant subsidiary and general ledger accounts. A cash receipts journal is a special journal used to record cash received by a business from any source. As these accounts are posted, the account number is entered into the post reference column. In the subsidiary ledger, the post reference is “CR-8”, which indicates that the entries came from page 8 of the cash receipts journal.

- The length of time you should keep a document depends on the action, expense, or event the document records.

- Our mission is to empower readers with the most factual and reliable financial information possible to help them make informed decisions for their individual needs.

- In these cases, you will need to make a separate cash received journal entry to record this information.

- The cash receipt is then allocated to the appropriate revenue account, such as sales or service fees, or applied against a customer’s accounts receivable balance if it’s a payment for an earlier invoice.

Balance Sheet

You must also track how these payments impact customer invoices and store credit. To make sure you have cash receipt accounting down pat, check out the cash received journal entry examples below. You record cash receipts when your business receives cash from an external source, such as a customer, investor, or bank. And when you collect money from a customer, you need to record the transaction and reflect the sale on your balance sheet. When you collect money from a customer, the cash increases (debits) your balance sheet.

The cash receipt journal has many advantages about its use within regular business accounting methods. A cash receipts journal provides an easy and organized way to record all the cash receipts during the period. Therefore, it allows a quicker and accurate way to prepare the cash ledger and a cash flow statement for the business for an accounting period. Credit sales are not recorded in this accounting journal because there isn’t any cash collected in those credit sales transactions.

Learn How to Record in a Sales Journal Exercise 7-1

This can cause the customer’s account to be inaccurate and may result in the customer being overcharged or undercharged. All cash receipts for a given accounting period are recorded in the cash receipts journal, a special kind of accounting journal. Cash receipts, on the other hand, serve as documentation of a cash sale from the cash received for your company.

A column for the transaction date, account name or customer name, invoice number, posting check box, accounts receivable amount, and cost of goods sold amount. Since all sales recorded in the sales journal are paid on credit, there is no need for a cash column. A common error made when posting entries from a cash receipts journal is to forget to post the individual amounts in the accounts receivable column to the subsidiary ledger accounts receivable.

The cash book is a chronological record of the receipts and payments transactions for a business. A special journal (or specialized journal) used to record money received. In a manual systemthis will allow one entry to the Cash account for the month (or shorter periods) instead ofdebiting the Cash account for every receipt.

This summary is ordinarily made in your business books (for example, accounting journals and ledgers). Your books must show your gross income, as well as your deductions and credits. As before the first three columns in the diagram are the date, transaction description (Desc.), and ledger folio reference (LF). The two columns referred to in the name of this cashbook are the monetary amount of the cash receipt (Cash), and the monetary amount of the receipts into the current bank account of the business (Bank), both highlighted in gray. For example, when a company purchases merchandise from a vendor, and then in turn sells the merchandise to a customer, the purchase is recorded in one journal and the sale is recorded in another.

In addition to these general guidelines, each business should consider any industry standards which may affect the holding period of records due to the unusual legal circumstances. Chartered accountant Michael Brown is the founder and CEO of Double Entry Bookkeeping. He has worked as an accountant and consultant for more than 25 years and has built financial models for all types of industries. He has been the CFO or controller of both small and medium sized companies and has run small businesses of his own. He has been a manager and an auditor with Deloitte, a big 4 accountancy firm, and holds a degree from Loughborough University. Let’s say you own a cute little toy store and have many regular customers.

When a piece of merchandise or inventory is sold on credit, two business transactions need to be record. First, the accounts receivable account must increase by the amount of the sale and the revenue account must increase by the same amount. Second, the inventory has to be removed from the inventory account and the cost of the inventory needs to be recorded. So a typical sales journal entry debits the accounts receivable account for the sale price and credits revenue account for the sales price.